Published:22 July 2024

This Article was Written by: Chris Proudfoot - Fundhouse

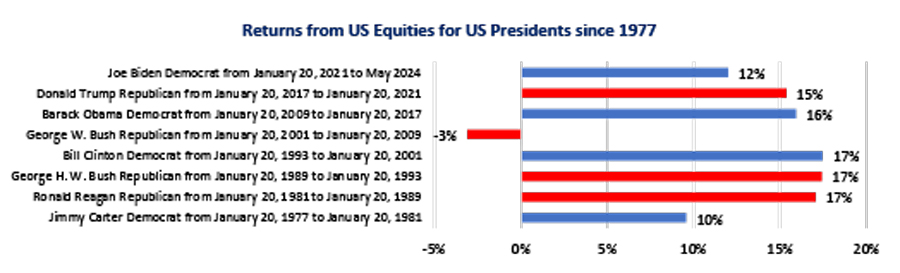

2024 US Election, Market Insights

This Article was Written by: Chris Proudfoot - Fundhouse

2024 US Election, Market Insights

Spring Statement 2025

Pre-budget media coverage has focused on the government’s ‘fiscal headroom’ – the leeway that Chancellor...

High Yield - Views and Positioning

‘High yield’ is a distinct asset class that sits at the higher credit risk end of the bond market.

February 2025 Economic and Market Report

In February, we learned that UK consumer prices had risen by 3% over the 12 months to January, up from...

Recent Market Volatility

These are certainly interesting times to invest, with worrying and persistent headlines

Are We in a Stock Market Bubble?

The four most dangerous words in investing are: ‘this time it’s different’ Sir John Templeton, 1993....

January 2025 Economic and Market Report

In January, we learned that consumer prices in the UK rose by 2.5% in the 12 months to December; a number...

Tech Turbulence: AI Disruptors

On Monday, Nvidia experienced a sharp decline of 16.9%. The sell off happened on the back of news that...

Understanding Gilt Yields

Gilt yields have recently been the subject of news interest. But, looking through the noise, are gilts...

December 2024 Economic and Market Report

In December, we learned that consumer prices in the UK rose by 2.6% in the 12 months to November, up...

Financial Services Industry 2024 Review

This report draws on our independent fund research and in-depth insights into the financial services...